What is Blockchain technology?

“It can be compared to a decentralized ledger where each transaction is recorded in a transparent, accessible, and secure manner.”

Reading time : 7min

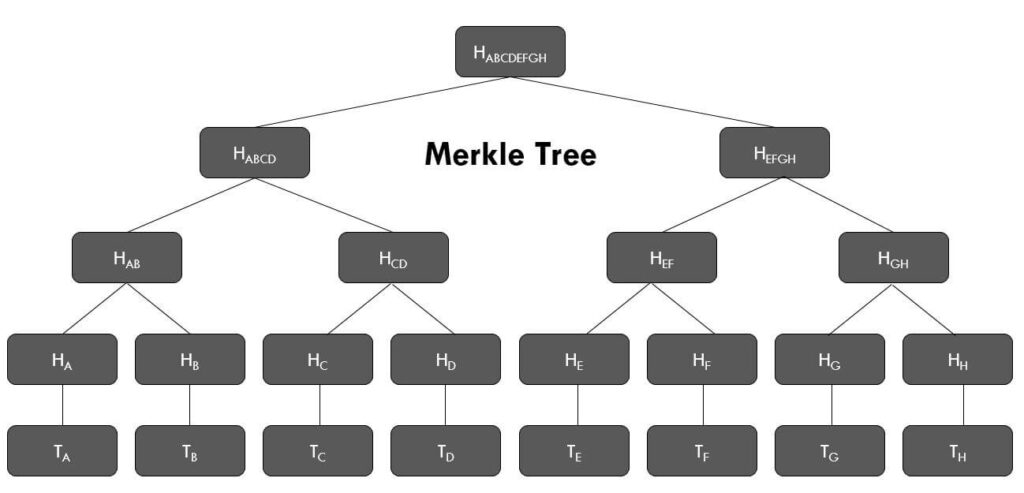

Blockchain is a technology that gained significant traction in the 21st century, much like artificial intelligence. However, its origins date back to the 1980s and 1990s with the foundational work of researchers such as Haber and Stornetta, who introduced key concepts like Merkle trees.

Source : https://o3schools.com/merkle-trees-and-merkle-roots/

It can be compared to a decentralized ledger where each transaction is recorded in a transparent, accessible, and secure manner.

Thanks to blockchain, cryptocurrencies like Bitcoin were created, but its potential extends far beyond digital currency. It is now applied across many sectors, offering a robust solution to the well-known trilemma of security, transparency, and decentralization.

This article explains how blockchain works, why it matters, and how it is already being used in everyday life. Whether you’re new to the subject or already familiar, this guide offers the essentials you need to better understand blockchain.

Definition: An immutable and decentralized database

A blockchain is a secure digital ledger that multiple users can access and that records every transaction carried out on a network. Unlike traditional databases, it cannot be changed or tampered with unless the entire network agrees to it, thanks to its decentralized nature.

Simplified example:

Imagine a shared accounting notebook accessible to thousands of people worldwide. Each new “page” (or block) contains verified transactions, and in networks like Bitcoin, a new block is validated approximately every 10 minutes.

Once a block is added to the chain, it cannot be modified or deleted. In theory, someone could attempt to take control of a blockchain like Bitcoin, but due to the network’s size, decentralization, and the immense computational cost, this is virtually impossible.

This structure ensures full traceability and transparency, significantly limiting fraud or manipulation, even though theoretical risks always remain.

How blockchain works

1. A chain of linked blocks

Blockchain is made up of a sequence of blocks, each containing:

- A list of validated transactions (such as cryptocurrency transfers, property title updates, smart contract executions)

- A unique hash from the previous block, linking them together

- A new hash that secures its position in the chain

Why it matters:

If someone tries to alter one block, they would have to modify every block that follows. This makes tampering extremely difficult and impractical.

2. A decentralized network without intermediaries

Blockchain operates without central intermediaries. Unlike banks or government authorities, no central entity controls it. This decentralized nature is why cryptocurrencies are often described as “people’s money” or a store of value.

The network relies on nodes (computers) that validate transactions and maintain network security.

Real-world example:

A traditional bank transfer goes through several intermediaries, each applying fees. In contrast, a blockchain transaction is verified directly by the network. One can transfer large amounts, such as one million dollars in Bitcoin, within seconds, with minimal fees and no third-party validation required.

Outcome:

Transactions are faster, more cost-effective, and more secure.

3. Transaction validation through consensus

For a block to be added to the blockchain, the network must agree on its validity. This is done through what is called a consensus mechanism.

Two major methods exist:

- Proof of Work (PoW):

Used by Bitcoin, this method requires solving complex mathematical puzzles (mining). Miners use computational power to validate transactions, ensuring decentralized network security. - Proof of Stake (PoS):

Used by Ethereum 2.0, PoS selects validators based on the number of tokens they hold and are willing to “stake.” It allows individuals to participate in securing the network without the need for expensive hardware.

Why it matters:

These systems protect the network, verify transactions, and prevent fraudulent activity, making the blockchain a trusted and immutable environment.

Benefits of blockchain technology

- Security: Once added, transactions are permanent and cannot be altered.

- Transparency: All activity can be audited on public blockchains.

- Decentralization: No single entity has control over the network.

- Automation: Smart contracts execute specific actions automatically when conditions are met.

Practical applications of blockchain

Financial Transactions and Cryptocurrency

- Bitcoin and Ethereum allow individuals to send money without using a bank.

- Stablecoins like USDT and USDC offer price stability by being pegged to traditional currencies.

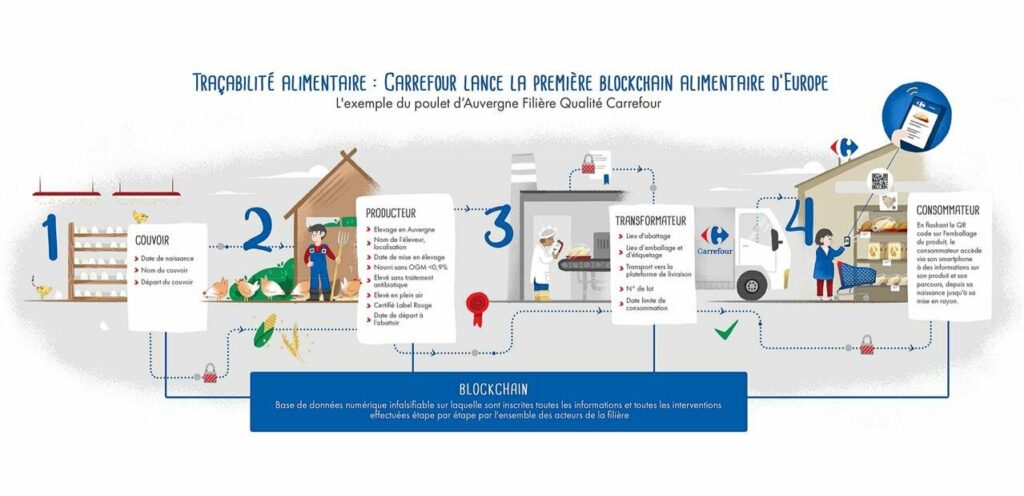

Supply chain and logistics

- Carrefour and IBM use blockchain to track food supply chains.

- Walmart uses blockchain to trace the origin of its fresh produce.

Source : https://next.ink/brief_article/carrefour-mise-sur-la-blockchain-pour-son-nouveau-programme-de-tracabilite-quelles-garanties/

NFTs and digital art

- NFTs allow digital creators to monetize their work while ensuring authenticity and ownership.

- Platforms like OpenSea enable users to trade unique digital assets.

Healthcare

- Blockchain ensures the secure and private storage of medical records.

- It facilitates data sharing between professionals while preventing tampering.

Real Estate and tokenization

- In Spain, a property was successfully sold as a token on a blockchain.

- Tokenization enables fractional ownership, allowing more investors to access real estate markets.

For more on tokenization, you can find our article and our YouTube video on the subject.

Challenges and limitations

- Energy consumption: PoW networks like Bitcoin consume high levels of electricity, though newer PoS systems are much more efficient.

- Scalability: During peak usage, some blockchains experience delays. Emerging technologies aim to improve this by balancing speed, security, and decentralization.

- Regulation: Governments are working on frameworks to combat fraud and ensure user protection, similar to traditional financial systems.

- Complexity: Adoption in traditional industries remains a challenge due to technical barriers and integration costs, though the long-term benefits are considerable.

Conclusion: A technology in motion

Blockchain is reshaping how we manage value and information across the globe.

Though still evolving, its growing adoption in finance, healthcare, supply chain management, and digital services proves that it is more than just a tool for cryptocurrency.

As innovation continues, one key question remains:

How long before blockchain becomes embedded in everyday life?

Have you ever used a blockchain-based service?

Feel free to share your experience or thoughts in the comments.

Sources

- French Ministry of Economy – Definition and Applications of Blockchain

- Coin Academy – Differences Between Bitcoin and Blockchain

- AWS – What is Blockchain?

- ETC Group – Blockchain Technology

💬 Subscribe now to stay informed about the latest cryptocurrency regulations and Web3 trends!